Categories

BuyerPublished April 12, 2026

Down Payment on a $300K Home in Davenport, FL Explained

How Much Do You Really Need for a Down Payment on a $300K Home in Davenport, FL? (Full Breakdown by Loan Type)

If you're eyeing a $300,000 home in Davenport, Florida, the down payment question is usually the one keeping you up at night. You've probably heard everything from "you need 20% down" to "you can buy with nothing down," and both answers leave you more confused than when you started. The real number depends on the loan you qualify for, your credit profile, and how much cash you want to keep in the bank after closing.

As a Davenport FL REALTOR working with buyers across Polk County and the broader Central Florida real estate market, I'll walk you through the actual down payment ranges for a $300K home, what each option truly costs out of pocket, and how to decide which one protects your long-term wealth. Before we go deeper, if you haven't run your numbers yet, start with a clear look at how much home you can really afford in Davenport, FL so the down payment conversation is anchored to a realistic budget.

The Short Answer: Down Payment Ranges on a $300,000 Davenport Home

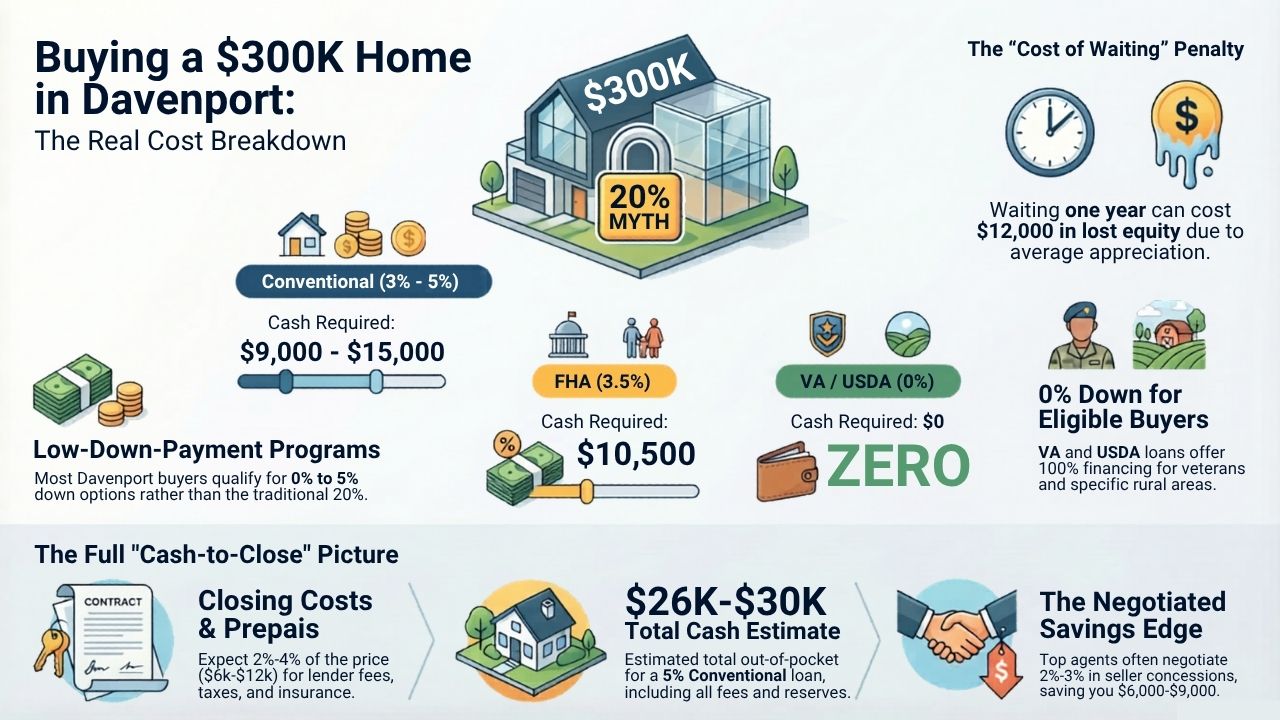

Here is the quick math based on the most common loan programs available in Davenport, Champions Gate, Celebration, Kissimmee, Orlando, and Four Corners:

- Conventional (3% down): $9,000

- Conventional (5% down): $15,000

- FHA (3.5% down): $10,500

- VA loan (0% down, eligible veterans): $0

- USDA loan (0% down, eligible rural areas): $0

- Conventional (10% down): $30,000

- Conventional (20% down): $60,000

Those numbers are just the down payment. They do not include closing costs, prepaids, or reserves, which we'll cover in detail below.

What Happens If You Assume 20% Is the Only Option?

This is the most expensive mistake I see buyers make in the Davenport market. They assume they need $60,000 in cash, decide they can't buy yet, and wait two or three more years while prices and rents keep climbing. During that time, they lose the home equity they could have been building.

The truth is that most first-time buyers in Polk County close with 3% to 5% down using conventional financing or 3.5% down using FHA. You can absolutely put 20% down if you have it and want to skip mortgage insurance, but treating it as a requirement is a myth that costs real families real money.

The Real Cost of Waiting

If a $300,000 home in Davenport appreciates even 4% next year, that's $12,000 in home equity you missed out on. Add another year of rent payments at $2,000 to $2,400 per month, and the cost of waiting to save a larger down payment often outweighs the savings.

Down Payment by Loan Type, Explained

Each loan program has different requirements, and picking the right one is just as important as the down payment itself.

Conventional Loans (3% to 20% down)

Conventional is the most flexible program and the most common for buyers in Davenport, Champions Gate, and Celebration. With credit around 680 or higher, you can qualify for 3% down through programs like Fannie Mae HomeReady or Freddie Mac Home Possible. Private mortgage insurance applies until you reach 20% equity, but it drops off automatically once you do.

On a $300K home at 5% down, you're looking at $15,000 for the down payment plus PMI that typically runs $100 to $200 per month depending on your credit score.

FHA Loans (3.5% down)

FHA is a strong option for buyers with credit scores between 580 and 679 or those with a thinner credit file. Down payment on a $300K home is $10,500. The tradeoff is mortgage insurance that stays for the life of the loan in most cases, so many buyers refinance into a conventional loan later once they've built equity.

VA Loans (0% down)

If you're an eligible veteran, active-duty service member, or qualifying spouse, the VA loan is almost always the best option available. Zero down payment, no monthly mortgage insurance, and competitive interest rates. A funding fee applies, but it can be rolled into the loan.

USDA Loans (0% down)

Parts of Polk County and the outer edges of the Four Corners area still qualify for USDA financing, which allows 100% financing for buyers who meet income limits. Not every home in Davenport qualifies, so your buyer agent Davenport FL needs to check the property address against the USDA eligibility map before you fall in love with a house.

What's the First Thing to Do Before You Decide on a Down Payment?

Before you pick a percentage, you need to know what you actually qualify for. That's where a real pre-approval conversation matters, not a 10-minute online estimate. A lender will review your credit, income, debts, and reserves, then tell you the loan programs you qualify for and the monthly payment at each down payment level.

Read this next to avoid the most common misstep: should you get pre-approved before buying a home in Davenport, FL?

Ready to See What You Can Afford?

Run your numbers in a few minutes with the Affordability Calculator to see what monthly payment fits your life before we start looking at homes on the MLS.

Down Payment Isn't the Only Cash You Need

This is where a lot of buyers get blindsided at the closing table. On a $300,000 home in Davenport, you should plan for more than just the down payment.

Closing Costs

Buyer closing costs in Polk County typically run 2% to 4% of the purchase price. On a $300K home, that's roughly $6,000 to $12,000. These include lender fees, title insurance, appraisal, survey, recording fees, and prepaid items like property taxes and homeowners insurance.

Prepaids and Escrow Reserves

Your lender will require you to prepay several months of property taxes and homeowners insurance into an escrow account. In Florida, homeowners insurance has climbed significantly, and that prepaid amount can surprise buyers who weren't warned in advance.

Post-Closing Reserves

Smart buyers keep two to six months of mortgage payments in savings after closing. Job changes, hurricanes, AC repairs, and life in general don't pause because you just bought a house.

Realistic Cash-to-Close Example on a $300K Davenport Home

Using 5% down conventional:

- Down payment: $15,000

- Closing costs: $8,000 to $10,000

- Prepaids and escrow: $3,000 to $5,000

- Total cash to close: roughly $26,000 to $30,000

Knowing this number in advance is the difference between a smooth closing and a panicked last-minute scramble.

How a Top REALTOR in Davenport FL Saves You Money on Your Down Payment

Here's what most buyers don't realize. The down payment conversation is only one piece of the structure of your offer. A top REALTOR negotiates seller concessions, interest rate buydowns, and closing cost credits that reduce the cash you bring to the table. On a $300,000 purchase, a well-negotiated concession of 3% puts $9,000 back in your pocket.

Want to see how that plays out in real deals? Here's a deeper look at interest rate buydowns and closing credits explained.

That kind of negotiation requires local knowledge of the Central Florida real estate market, a sharp read of comparable sales, and a Comparative Market Analysis (CMA) that supports your offer. It's the difference between paying full price with no help and buying smart with the seller covering a meaningful chunk of your costs.

Is Now a Good Time to Buy in Davenport, FL With a Low Down Payment?

In the current Davenport market, inventory has expanded, sellers are more willing to negotiate, and interest rates remain high enough that creative financing structures, rate buydowns, and concessions are actively on the table. That's a favorable environment for low-down-payment buyers who structure their offers well.

Waiting for "perfect" rates or "perfect" prices usually costs more than acting with a smart strategy today. A buyer consultation clarifies your specific situation, timeline, and target neighborhoods so you move with confidence instead of guesswork.

Frequently Asked Questions

Can I buy a $300K home in Davenport with less than $10,000?

Yes, if you qualify for a VA or USDA loan with 0% down, your out-of-pocket cost is mostly closing costs and prepaids, which can sometimes be covered through seller concessions or lender credits. With FHA at 3.5% down, you'll need closer to $18,000 to $22,000 total cash to close. A lender can confirm your exact numbers in a pre-approval call.

Is PMI really that bad on a conventional loan?

PMI adds $100 to $250 per month on a $300K home at 5% down, but it drops off automatically once you reach 20% equity. Many buyers reach that threshold within a few years through appreciation and principal paydown, making PMI a short-term cost rather than a permanent one. For the right buyer, putting less down and keeping cash in reserves is smarter than stretching for 20%.

What credit score do I need for the best down payment options?

For conventional 3% down programs, aim for 680 or higher. FHA allows scores as low as 580 with 3.5% down. VA and USDA loans typically look for 620 and up, though some lenders go lower. If your score is borderline, a 30 to 60 day credit improvement plan before applying can save you thousands over the life of the loan.

Can the seller pay part of my down payment in Davenport, FL?

Sellers cannot pay your down payment directly, but they can contribute to closing costs, prepaids, and interest rate buydowns, which frees up your cash for the down payment. In the current Davenport market, seller concessions of 2% to 3% are common and actively negotiated. This is one of the highest-leverage moves a buyer agent Davenport FL can make for you.

Should I wait and save 20% or buy now with less down?

In most cases, buying now with less down builds home equity faster than waiting and saving. Between appreciation, principal paydown, and the rent you stop paying, the math usually favors buyers who act with the right loan and strategy. Run your own numbers against local rent and appreciation trends before deciding.

Your Next Step

If you're serious about buying a $300,000 home in Davenport, Champions Gate, Celebration, Kissimmee, Orlando, or Four Corners, the next move is simple. Get your numbers mapped, your loan options compared, and your buying strategy built around the cash you actually have, not the cash someone told you that you need.

Let's connect for a no-pressure buyer consultation. I'll walk you through loan options, local listings, realistic cash-to-close scenarios, and a listing strategy that fits your goals, so you close on the right home with the right numbers.

{ "@context": "https://schema.org", "@type": "Article", "headline": "How Much Do You Really Need for a Down Payment on a $300K Home in Davenport, FL? (Full Breakdown by Loan Type)", "author": { "@type": "Person", "name": "Manny Barrios", "jobTitle": "REALTOR", "url": "https://www.2mannyhomes.com/agent-profile/manny-barrios-137118674" }, "publisher": { "@type": "Organization", "name": "2MannyHomes" }, "locationCreated": { "@type": "Place", "name": "Davenport, Florida", "address": { "@type": "PostalAddress", "addressLocality": "Davenport", "addressRegion": "FL", "addressCountry": "US" } }, "keywords": "down payment Davenport FL, Davenport FL REALTOR, $300K home Davenport, FHA loan, conventional loan, buyer agent Davenport FL", "datePublished": "2026-04-12", "description": "A full breakdown of down payment requirements on a $300,000 home in Davenport, FL by loan type, including conventional, FHA, VA, and USDA, plus closing costs and real cash-to-close scenarios." }

|

or another way